On 28th October 2016, the application for the judicial approval (homologación judicial) of the Restructuring Agreement was filed with the Mercantile Courts of Seville. The judicial approval of the agreement was issued on 8th November 2016.

During the accession period that finalized on 25th October, the Restructuring Agreement received the support of 86% of the financial creditors to which it was addressed, exceeding the legally required majorities (75%).

During the Extraordinary Shareholders’ Meeting that took place on 22nd November 2016, all proposals related to the Restructuring Agreement were approved achieving another critical milestone in the restructuring process started in November 2015.

As a result of the Supplemental Accession Period that was open in January, accession to the Restructuring Agreement has increased to a total of 94% of the financial creditors to which it was addressed.

The company announced on March 31, 2017 through a Significant Event with the CNMV (Hecho Relevante) that it had achieved the completion of the financial restructuring. Those creditors that failed to adhere to the Restructuring Agreement to date will no longer be allowed to so.

The new notes and shares that were issued in accordance with the Restructuring Agreement were transfered to the Clearing Systems on the week of March 27th. In general, all securities were credited to the corresponding noteholders on March 31st. If you have not received your securities yet please contact your custodian bank so that they can claim them from the clearing systems. Abengoa does not participate in the process.

If you are a noteholder, you should have Access to the relevant documentation on the dataroom provided by Lucid:http://lucid-is.com/abengoa/rdad/

A summary of the main terms and conditions can be found in the following document: New bonds - overview of key terms

The financial restructuring was completed on March 31, 2017. Those creditors that failed to accede to the Restructuring Agreement during the established phases (the Initial Accession Period in October 2016 or the Supplemental Accession Period in January 2017), will not have another opportunity to do so. As per the terms of the Restructuring Agreement and consequence of its judicial homologation, those creditors will be applied the Standard Restructuring Terms as described in question 8 below.

As was the case during November 2016, Abengoa’s creditors are required to vote in favour of an additional Chapter 11 process in the United States, the purpose of which is to apply the homologation of the Standard Restructuring Terms to entities that do not accede to the Restructuring Agreement with respect to their claims against certain US affiliates.

The accession period is opened until 18th April 2017 at 18.00 CET.

Voting mechanics will be similar to previous processes, through an instruction to be sent by your custodian entity where your bonds are held.

For bonds deposited at Euroclear/Clearstream: through electronic instruction indicating their vote in favour (“Accept the Plan”) or against (“Reject the Plan”). If you have any questions regarding the voting process you can contact Lucid Issuer Services on abengoa@lucid-is.com

For bonds deposited at DTC: noteholders to complete the Beneficial Holder Ballot, indicating their vote in favour (“Accept the Plan”) or against (“Reject the Plan”) and send to their custodian. In order to obtain the documentation or solve any queries you can contact the agent Prime Clerk on abengoaballots@primeclerk.com

According to Article IX.B.2 of the plan, when voting in favour the bondholder is waiving their right to take any legal action related to the Chapter 11 process. If one does not want to waive this right it should be specified when sending the vote (exact wording could change depending on how the instruction is received by custodians but it should make a reference to “releases contained in article IX.B.2 of the plan”)

It should be taken into account that custodian entities might set earlier voting deadlines than 18th April, so we recommend to get in touch with them as soon as possible.

Finally, we would like to remind you that as per clause 9 of the Restructuring Agreement, those bondholders that have acceded to the same are contractually obligated to vote in favour of this Chapter 11 proceedings.

The financial Restructuring Agreement constitutes the necessary grounds to achieve a sustainable capital structure in order to allow Abengoa to restart its operations and to preserve stakeholder’s value avoiding a potential liquidation scenario.

The total financial commitments amount to 1,170 million euros of new money plus 307 million euros of new bonding lines enabling Abengoa to reinitiate normalised operations.

The new capital structure of the company shall consist of:

The aforementioned agreement shall, in any event, be subject to a number of conditions that include, among others, reaching the percentage of accessions by the creditors required by law.

All of Abengoa bonds are part of the debt subject to the aforementioned agreement that stipulates a new set of conditions for current bondholders.

The Standard Restructuring Terms for the preexisting debt will involve a debt reduction of 97% of its nominal value, while keeping the remaining 3% with a ten-year maturity, with no annual coupon and no option for capitalization.

Creditors who adhere to the agreement shall have the option to choose the Alternative Restructuring Terms, which consist of the following:

- 30% of the nominal value of outstanding debt (for a bond of 100.000€ nominal value, the new principal amount would be 30.000€) to be converted into a new bond or loan, that will rank as senior or junior depending on whether or not bondholders participate in the new money facilities, with the following terms:

- Option to capitalize the remaining 70% of the nominal value of outstanding debt (for a 100.000€ bond, the amount would be 70.000€) in exchange for 40% of Abengoa’s shareholders equity post restructuring, which would be proportionally distributed among existing financial creditors. The monetary value of such stake will only be determined once the required capital increase has been completed.

A presentation providing an overview of the updated Abengoa Viability Plan and the summary terms of the Restructuring Agreement was presented to the market on August 16th 2016 and is available on Abengoa’s website.

As mentioned before, a Supplemental Accession Period will be opened in the coming weeks during which, those noteholders that did not do so during the initial period, will be able to choose the terms of the restructuring of their debt positions. Specifically, bondholders will have to elect the following:

- The Standard Terms or the Alternative Terms explained in the previous question.

- Under the Alternative Terms of the restructuring, bondholders should choose from:

- Whether or not they will be participating in the New Money facilities.

For clarification purposes, should the Restructuring Agreement be homologated in court, the Standard Restructuring Terms will be applied to those bondholders that did not accede to the agreement.

The current accession process for the Restructuring Agreement is described in the following questions.

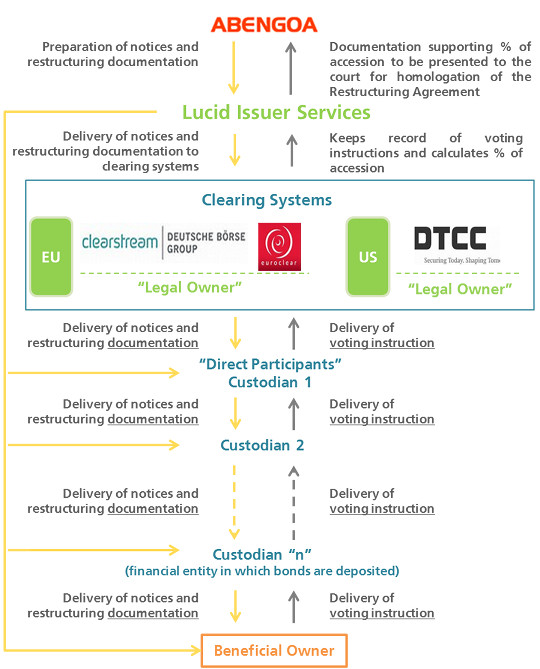

To ensure the integrity of the accession process, Abengoa has retained Lucid Issuer Services (‘Lucid’) in the role of tabulation agent that will be in charge of sending all necessary documentation to the clearing systems and keep record of the voting instructions received. For illustrative purposes, a simplified representation of the voting process is as follows:

1) Lucid Issuer Services1): is the “tabulation agent” in charge of the delivery of the documentation for the restructuring process and related notices through the clearing systems. Lucid will also keep record of the votes from the noteholders and will calculate percentages of accession to the Restructuring Agreement.

2) Clearing Systems: systems established to facilitate capital market transactions (payments, transfer of ownership of securities). In this particular case, they are the means through which all documentation related to Abengoa’s restructuring process will be distributed to reach the final beneficial owner through the chain of custodian entities. They also keep record of the legal owners of the bonds.

3) “Legal owner”: entities registered in the clearing systems as the holders of the bonds for legal purposes. Notwithstanding the fact that beneficial owners have the right to make the voting decision, it is the legal owners that have to ultimately cast the vote.

4) Custodian 1 (“Direct Participants”): first entities on the chain of custodians that hold accounts directly in the clearing systems.

5) Custodian “n”: the chain of custodians has a variable number of entities between the direct participants and the final custodian to the beneficial owners. Custodian #”n” holds the bonds for the beneficial owner and should assist in the accession process.

6) Beneficial Owner: it is the bondholder that ultimately has to make a decision with respect to the Abengoa’s financial Restructuring Agreement, and with the help of the custodian entity (custodian “n”) get the vote channeled through the system and registered.

The voting process will be as follows:

1) Lucid, on behalf of Abengoa, sends all notices and documentation related to the restructuring agreement to the clearing systems.

2) The clearing systems inform and distribute the documentation to the entities that are “Direct Participants”.

3) Documentation flows down the chain of custodians until it reaches the beneficial owner (bondholder)

4) The voting instruction given by the beneficial owner flows back the same chain of custodians and clearing systems until it reaches Lucid.

5) Lucid keeps records and provides accession percentages to Abengoa.

As indicated in the process previously described, Abengoa’s bondholders should get in touch with their custodians, the financial entities where their bonds are deposited, for them to assist in the whole process, from the request of documentation to the delivery of the voting instructions.

In this specific situation, and with the purpose of expediting the process, bondholders will be able to get the restructuring agreement documentation directly from Lucid (abengoa@lucid-is.com). Under no circumstances will the delivery of the voting instructions be done directly with Lucid or any other mechanism different to the one described above, as the votes must be formally delivered by the legal owners described previously.

In this process, the cooperation of the custodian financial entities is not only advisable but it is essential, otherwise bondholders will not be able to exercise their rights.

All existing creditors at the signing date have the right to participate in the New Money Financing, the terms of which are explained in the Restructuring Agreement and Abengoa’s presentation of 16th August 2016.

1. Process: in order to participate in the New Money Financing, creditors must:

2. Options: in the form creditors must indicate:

3. Amount:

4. Elevation:

5. Deadline:

Houlihan Lokey is acting as bookrunner of the New Money process, and they can be contacted on abgnotes@hl.com. Lucid Issuer Services is not involved in this part of the process.

From Abengoa we are committed to keep you updated on the developments of the restructuring process; however, for advice on the management of your investment you should consult your own professional investment advisor.

If at any point you have additional questions, you can contact us on:

Abengoa

Telephone: +34 954 937 000

Via email by filling out the following form:

Bondholders’ Office